Hong Kong’s new Open-Ended Fund Company regime

Hong Kong brought its new open-ended fund company (OFC) corporate structure into force on 30 July 2018, after four years of market consultation and draft legislation. Part of the government strategy to strengthen Hong Kong’s almost HK$20 trillion fund management industry, the OFC provides a corporate structure similar to that of the UK’s Open-Ended Investment Company and Singapore’s imminent Singapore Variable Capital Company.

The OFC benefits investors and fund managers alike by providing the investor protection and familiarity of a company limited by shares and by also simplifying the raising of funds. Previously this was limited to the more complex fund structure of a unit trust in Hong Kong.

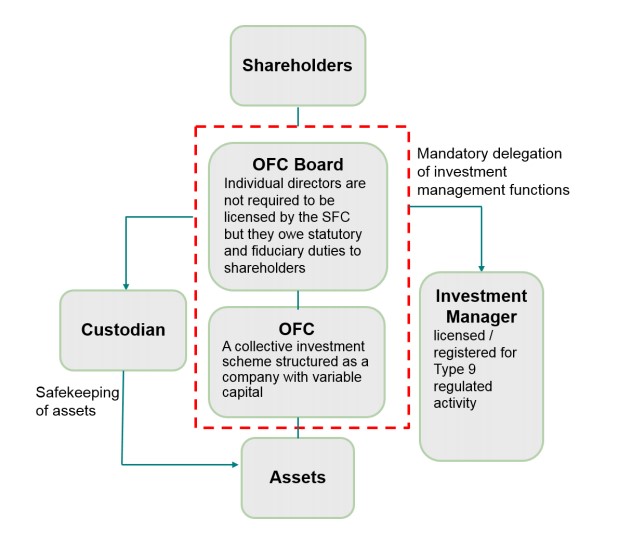

An OFC is an open-ended collective investment scheme that is intended to operate as an investment fund vehicle managed by a professional investment manager. It is set up in the form of a limited liability company but with the flexibility to create and cancel shares for investors’ subscriptions and redemptions.

The key features of an OFC are as follows:

- It may be offered either publicly or privately

- It has a variable share capital structure with flexibility to meet subscription and redemption requests and pay distributions with net assets/capital

- It may be used as a collective investment vehicle either as a standalone entity, or as an umbrella entity with separately pooled sub-funds

An OFC is established by obtaining registration from the Securities and Futures Commission (SFC) and a certificate of incorporation from the Companies Registry (CR). It must appoint at least two individual directors who are subject to fiduciary duties and the duty to exercise reasonable care, skill and diligence.

An OFC is also required to: have an investment manager that is licensed by or registered with the SFC to carry out asset management regulated activity; assign a custodian to whom all scheme property must be entrusted for safe-keeping; and appoint an auditor for each financial year. A solvent OFC may apply to the SFC for the termination of its registration under a streamlined process.

The Hong Kong government has supported the introduction of the new OFC by enacting the Inland Revenue (Amendment) (No. 2) Ordinance 2018 (IRAO). This extends the profits tax exemption currently enjoyed by publicly-offered funds and certain offshore privately-offered funds, to onshore privately-offered OFCs. By reducing the unequal tax treatment between overseas and domestic private funds, the IRAO seeks to encourage more private funds to domicile in Hong Kong.

OFCs have the added benefit of being a familiar investment vehicle for asset managers and regulators from non-Commonwealth jurisdictions such as mainland China and could be a popular vehicle for asset managers that are seeking to distribute investment products into the PRC under the Mainland-Hong Kong Mutual Recognition of Funds Scheme.

The operational advantage of using a Hong Kong-domiciled structure is that, unlike setting up funds in traditional fund jurisdictions like Cayman Islands, it circumvents the nuisance and costs of appointing additional service providers and dealing with overseas regulators. The new OFC regime will enable managers to deal with a single regulatory regime and with the SFC as the sole regulator.