Personal Service Company

The Situation

Mr C is a highly paid IT consultant who works throughout the world. Each project normally lasts at least six months and requires Mr C to travel to a foreign country to carry out his duties.

The Problem

Mr C is likely to spend more than six months in each country in which he undertakes a project and is therefore likely to become tax resident in that country and subject to that country’s full rate of tax on the income generated from the project. Mr C is normally resident in a low tax country and is therefore unwilling to pay higher levels of tax. Mr C also finds it difficult to be competitive when he quotes for a project unless he is tax efficient in the way that he works.

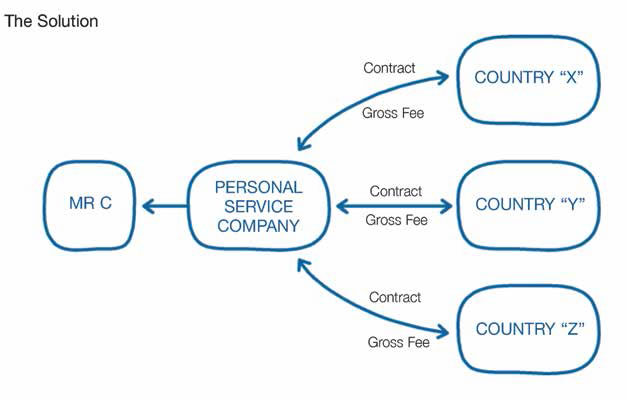

The Solution

Mr C should set up a personal service company. This company, rather than Mr C in a personal capacity, should enter into contracts with clients. If Mr C’s company is located in a jurisdiction that has a tax treaty with the country in which he carries out the work, payments can usually be made free of both withholding tax and tax at source. Mr C’s company can then pay him a moderate salary, leaving the balance of the contract value to be taxed at the company’s low rate.

Notes

Employment income may be taxable at source without the use of a tax treaty as described above. It is therefore important to select a jurisdiction that has low effective rates of tax but still manages to reduce any withholding tax or tax at source on the income paid. Malta, Cyprus and Mauritius may all provide planning opportunities here. Alternatively, structures using high tax countries such as UK Limited Liability Partnerships (LLPs) or US Limited Liability Companies (LLCs) may also provide a solution.