Cyprus – the ideal location for structuring investments in South Africa

Since the 1st of January 2021, South African resident individuals with authorised (also termed permissible) foreign assets may invest in South Africa, provided that where South African assets are acquired through an offshore structure, resulting in a loop structure, the investment must be reported to an Authorised Dealer (South African bank) as and when the transaction is finalised.

To ensure tax efficiency, it is important that the holding entity through which South Africans invest into South Africa, is incorporated or established in a jurisdiction that has entered into a double taxation agreement (“DTA”) with South Africa. It is for this reason that Cyprus’ popularity as a holding vehicle jurisdiction has increased significantly since the beginning of the year 2021. South Africa and Cyprus entered into a DTA which came into force on the 8th of December 1998. The DTA was amended in 2015. The key changes of the treaty relate to dividends tax and exchange of information.

Also important to highlight is the fact that the SA/Cyprus DTA gives Cyprus a significant advantage above other treaty jurisdictions of South Africa because of the fact that the gains on the sale of property rich companies owned by a Cyprus company are not taxed in SA (and neither is it taxed in Cyprus provided that the property is not situated in Cyprus). In terms of other DTA’s that South Africa has entered into the gains would usually be taxable in SA.

AMENDED SOUTH AFRICA – CYPRUS DTA MAIN PROVISION

- Withholding tax rate on dividends has been increased:

- A withholding tax rate of 5% will apply if the beneficial owner of the dividends is a company which

holds at least 10% in the share capital of the company distributing the dividends; and - A withholding tax rate of 10% will apply in all other cases (for example, when a Cyprus trust hold the shares of a SA company, the withholding tax on dividends payable to the Cyprus trust would be 10%.)

- A withholding tax rate of 5% will apply if the beneficial owner of the dividends is a company which

- Withholding tax rate on interest: 0%

- Withholding tax rate on royalties: 0%

- Capital gains tax: shares in a company owning movable or immovable property in the other jurisdiction are

taxed only in the country of which the seller of those shares is a resident. - Residence: The definition of “resident in Contracting State” is aligned with the 2014 OECD model treaty. For

purposes of the South Africa – Cyprus Double Tax Treaty, the term “resident of a Contracting State” means “any person who, under the laws of that State, is liable to tax therein by reason of his domicile, residence, place of management or any other criterion of a similar nature and also includes that State and any political subdivision or local authority thereof. This term, however, does not include any person who is liable to tax in that State in respect only of income from sources in that State.” Where a company is a resident of both South Africa and Cyprus, it shall be deemed to be a resident only of the State in which its place of effective management is situated. - Exchange of information – aligned with the 2014 OECD model treaty. The level of information that is expected

to be exchanged between the two States will be as much information as is foreseeably relevant.

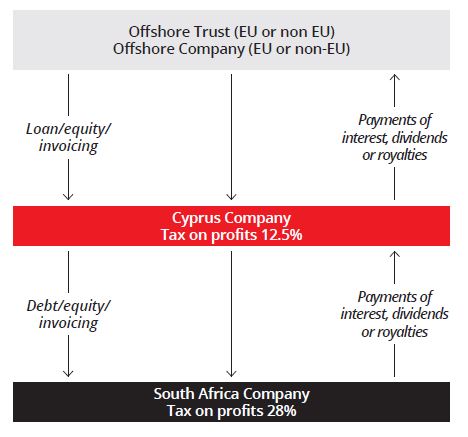

STRUCTURE – INVESTMENT IN SOUTH AFRICAN COMPANIES THROUGH A CYPRUS COMPANY

- 0% withholding tax on dividends in Cyprus

- 0% withholding tax on royalties in Cyprus

- 0% withholding tax on interest in Cyprus

- 5% withholding tax on dividends, provided that the Cyprus company holds at least 10% of the share capital in the SA company and is the beneficial owner of the dividend. In all other cases, the withholding tax rate would be 10%.

- 0% withholding tax on interest, provided that the Cyprus company is the beneficial owner of the interest.

- 0% withholding tax on royalties, provided

that the Cyprus company is the beneficial

owner of the royalties.

TAXATION OF A CYPRUS COMPANY

The main features of the Cyprus company tax regime are as follows:

- A uniform corporate tax rate of 12.5% is applied to all companies.

- Dividend income is exempt from tax in Cyprus. It is also exempt from the special defence contribution of 20%

provided that the company paying the dividend either engages directly or indirectly in activities that give rise to more than 50% non-investment income or the burden on the dividend paying company’s income is not lower than 5% irrespective of its source, provided certain conditions are satisfied. Credit for foreign tax suffered is given irrespective of the existence of a treaty. - Interest income is exempt from corporate tax, unless it is received in the ordinary course of business in which

case it is taxed like normal trade income. A special defence contribution of 30% is payable by tax residents but

credit is given for foreign tax suffered irrespective of the existence of a treaty. - Profit from the disposal of securities is exempt from tax in Cyprus.

- Profits of a permanent establishment maintained abroad by a Cyprus company are exempt from tax in Cyprus

subject to certain conditions. - There is no withholding tax on dividends, interest payment or royalty payments.