Purchasing Property

The Situation

These notes will necessarily be general because the correct structure to purchase a property will differ from country to country depending on the local tax system in the country where the property is situated. However certain general principles apply in most, if not all, countries.

The Problems

Irrespective of the nationality, domicile, place of residence and personal circumstances of the owner most countries will apply the following taxes:

- Estate Duty: local estate duty is normally charged on the value of the property upon the death of the owner

because the asset is situated within their borders. Most countries levy some form of estate duty or an equivalent

tax on the death of the owner of that property. - Capital Gains Tax: on resale of the property most countries charge a tax based upon the difference between the

acquisition price and the resale price. - Income Tax: all countries charge local taxes on income generated from the exploitation of the property e.g. any

rent received from the occupation of that property. The tax would apply irrespective of who rents the property

and how the rental is paid and local tax returns must be filed detailing that income. - Stamp Duty: most countries charge a sales tax based upon the total value of the property upon any subsequent

transfer. The rate of this transfer tax can vary from a negligible figure to amounts as high as 15% and this can

often be the highest cost incurred when selling property.

The Solution

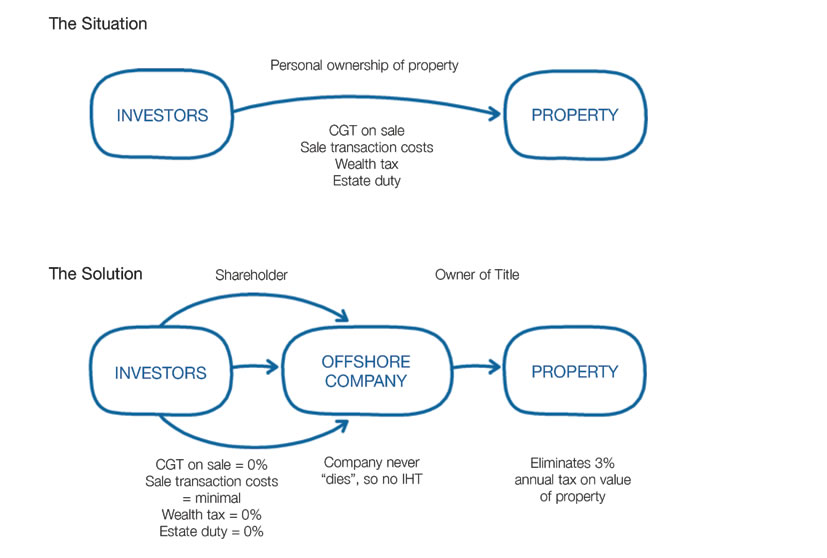

As a general rule, estate duty would be avoided if the property were to be owned by a company. This occurs because a company, unlike an individual, cannot “die” – thereby eradicating the estate duty that would be payable on the death of an individual. But many countries now charge estate duty on the worldwide assets of the owner. In this case the value of the shares – which would be equal to the value of the property – would be included in the estate of the deceased owner. In other words, although local estate duty may be avoided by corporate ownership, worldwide estate duty may not.

Even when loans are taken out against the value of the property, thereby reducing the value of the shares by the amount of the loan, either the loan itself or the assets that it has been used to purchase, may fall within the estate of the deceased. One way or another, the total value of the property is generally going to be “within the estate”. Further planning may therefore be necessary to minimise or eradicate the worldwide estate duty on the owner’s estate. Separate advice on this aspect will be needed.

If a company owns the property, then transferring the shares in the company may effect a transfer of ownership whilst leaving the title to the property unaltered. Some countries have initiated anti-avoidance legislation that treats the transfer of the shares in the property owning company as equivalent to a transfer in the property, and tax is charged accordingly. Those situations are rare and generally a sale of the shares will eradicate capital gains on the property. Again, the owner may be subject to capital gains on a worldwide basis, so further planning may be necessary to eradicate worldwide capital gains.

Income tax is charged on rental income but, generally, expenses incurred in producing the rent can be offset against the tax. Thus the maintenance costs of the property and the costs of any loan used to purchase the property, but not interest on loans raised against the property later – the interest payments – can be deducted from the rent before tax. The interest on a loan is usually by far and away the biggest allowable expense and, with careful planning, this can be used to minimise or totally eradicate local taxes on rental income. But note that all loans must be at arm’s

length terms for the interest to be allowable.

Corporate ownership also allows stamp duty, or other transfer taxes that would normally apply in the country where the property is situated, to be avoided. This is because a transfer of shares in an offshore company could generally be made without attracting such charges. Corporate ownership also allows easy division of the equity in a property, which enables the ownership to be rearranged without cost or expense.

It is common in many countries for property to change hands by way of a share transfer in the property owning company, so the vendor should readily find a buyer who will be comfortable with effecting the acquisition by way of a share transfer. It should be noted that any purchaser of shares in a company would, if subsequently obliged to sell the property out of the company, become liable to capital gains tax on the difference between the original purchase price and the current sale price. There is therefore a potential disadvantage in purchasing property through a transfer of shares, but generally it should be possible to calculate the potential worst case scenario, and for the buyer and seller to then

agree an equitable deduction in the purchase price by way of compensation.

In short, corporate ownership is a flexible way of owning property and maximising fiscal advantages, in all of the above-mentioned areas. However, careful planning is needed to avoid potential pitfalls, traps and specialist advice may need to be taken on fast changing tax legislation.